Mortgage Descriptions

Review the details below to learn more about what type of mortgage loan will work best for you,

Conventional Home Loans

1- to 4-unit primary residence

- 3% down payment for first-time home buyers; 5% for repeat buyers.

- 2% down payment assistance grant available for first time home buyers.

- Funds may be gifted/seller assists allowed

Vacation Homes

- 10% minimum down payment.

- Funds may be gifted/seller assists allowed.

- 15% minimum down payment for 1-unit homes. 25% minimum down payment for 2- to 4-unit homes.

- Must be deeded to the buyter. Cannot be deeded to an LLC.

Veterans Administration Loans

- 100% financing available. No cash reserve requirements

- No application fees

- No monthly mortgage insurance

- VA funding fee may be financed into the mortgage

- Funds may be gifted

Jumbo Loans

- Residential mortgage loans above $726,200

- Primary residence, vacation home, investment properties

- 10% minimum downpayment

- Cash reserves required

- Seller assists allowed up to 6%

FHA Loans

- Primary residence only

- 3.5% minimum downpayment

- Funds may be gifted/seller assists allowed

- Funding fee may be financed into mortgage

- Cash reserves may not be required

- 1- to 4-unit properties. Owner must occupy one unit.

USDA Home Loans

- Primary Residence /1 Unit

- 100% Financing

- Competitive Interest rates

- Cash Out Refinance not allowed

- Dwelling must be located in an eligible rural area

- Upfront 1% Guarantee fee may be financed into the mortgage

- Seller Assists up to 6% permitted

Commercial Real Estate Loans

- A Commercial real estate loan is a mortgage secured by a lien on a commercial property.

- They are generally made to investors such as corporations or organizations that own and operate commercial real estate.

- Commercial real estate loans are offered by banks, independent lenders, insurance companies, pension funds, private investors, and other capital sources.

- The Small Business Administration’s 504 Loan Program is a major source.

- Lenders consider the nature of the collateral (the property being purchased), the creditworthiness of the borrower, and financial ratios when evaluating commercial real estate loans.

- Commercial real estate loans have different rates and terms than residential mortgages.

- Investors who desire to deed residential properties in an LLC must finance using a commercial real estate loan.

New Construction Loans

- One closing

- One interest rate (with the option to modify down if the market improves)

- One down payment

- Available on conventional loans, including adjustable rate mortgages

- Minimum down payment

- Lender facilitates communication with the builder and provides you with checklists for the project approval and builder approval to help keep the approval process moving.

- No second approval needed. After the first approval, the borrower is good to go, helping to deliver a more seamless, efficient experience.

- Float down option. Once the loan is complete, borrowers can float down to secure a lower interest rate if the market changes or stay locked in no matter how the market moves.

- Initial interest-only payments. During the build period, the borrower can enjoy a lower, interest-only payment.

Less out-of-pocket expense. The borrower doesn’t have to pay for the build and then get a mortgage. The mortgage pays for the build.

Levels the playing field. Gives general contractors more freedom to build unique dream homes for their clients, rather than cookie-cutter developments.

Mortgage Resources

Today's Mortgage Rates

| ||||||||||||||||||||||||||||||||||||||||||

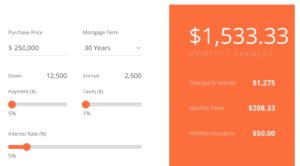

Mortgage Estimator

Click on the image to estimate your monthly mortgage payment based on your expected purchase price, interest rate and estimated taxes.